Over time, the performance of legacy banking applications has decreased significantly. Bugs, errors, and crucial problems arise, causing these apps to become so outdated that they no longer meet the demands of the digital age. With the rapid advancements in technology and the ever-increasing expectations of customers, it has become essential for banks to provide instant financial services, or else they switch.

Our experts understand the importance of banking app modernisation in the competitive market and can breathe new life into your legacy system to make it a frontrunner in the industry. Let’s explore how we have aided numerous BFSI enterprises in modernising their banking and financial apps successfully.

Benefits of Modernising a Legacy Banking System

Upgrading an outdated platform can be time-consuming and require substantial dedication, as it involves meticulous planning, careful analysis, and thorough testing. However, the benefits of legacy modernisation can outweigh them:

1. Innovative Digital Capabilities

Integrating emerging, cutting-edge software into older systems can be time-consuming, labour-intensive, and even impossible at a time.

By modernising legacy systems, banks can stay compatible with artificial intelligence (AI), machine learning (ML), big data, and open banking APIs, enabling them to innovate and offer new services that resonate with today’s tech-savvy customers.

2. Optimised Costs

As per McKinsey’s findings, medium-sized banks can potentially save $100 million by choosing progressive modernisation or transitioning to more advantageous digital banking options.

At first glance, transitioning your banking codebase to a modern alternative might seem costly. However, when considering the advantages, you’ll realise its substantial value due to the optimised costs when maintaining and addressing issues in modern banking apps.

3. Improved Customer Experience

Legacy-core banking systems often have obsolete user interfaces and features that lack responsiveness and optimisation for modern devices and browsers. This deficiency can lead to a poor user experience, particularly for those using digital channels such as mobile devices and web browsers to access banking services.

With modern systems in place, you can mobile banking app design and provide innovative features such as AI chatbots, cardless payments, personalised financial advice, etc. This enables you to provide a seamless and convenient banking experience to customers, ultimately improving customer satisfaction and loyalty.

4. Tighter Security

Relying on outdated infrastructure exposes your bank to security vulnerabilities. Due to their reliance on obsolete technologies, these systems become susceptible to breaches by hackers seeking to steal sensitive data or disrupt operations.

However, with a modern banking platform, you can utilise cutting-edge tools to handle security threats and swiftly respond to data breaches. Additionally, banks will get access to the progressive legacy systems that consider compliance regulations through their hybrid cloud delivery model.

Essential Steps for Modernising Banking Applications

To successfully modernise banking apps, banks and financial institutions need to follow a series of essential steps. This process ensures a smooth transition from legacy systems to modern systems, decreasing disruption to operations and maximising the benefits of modernisation.

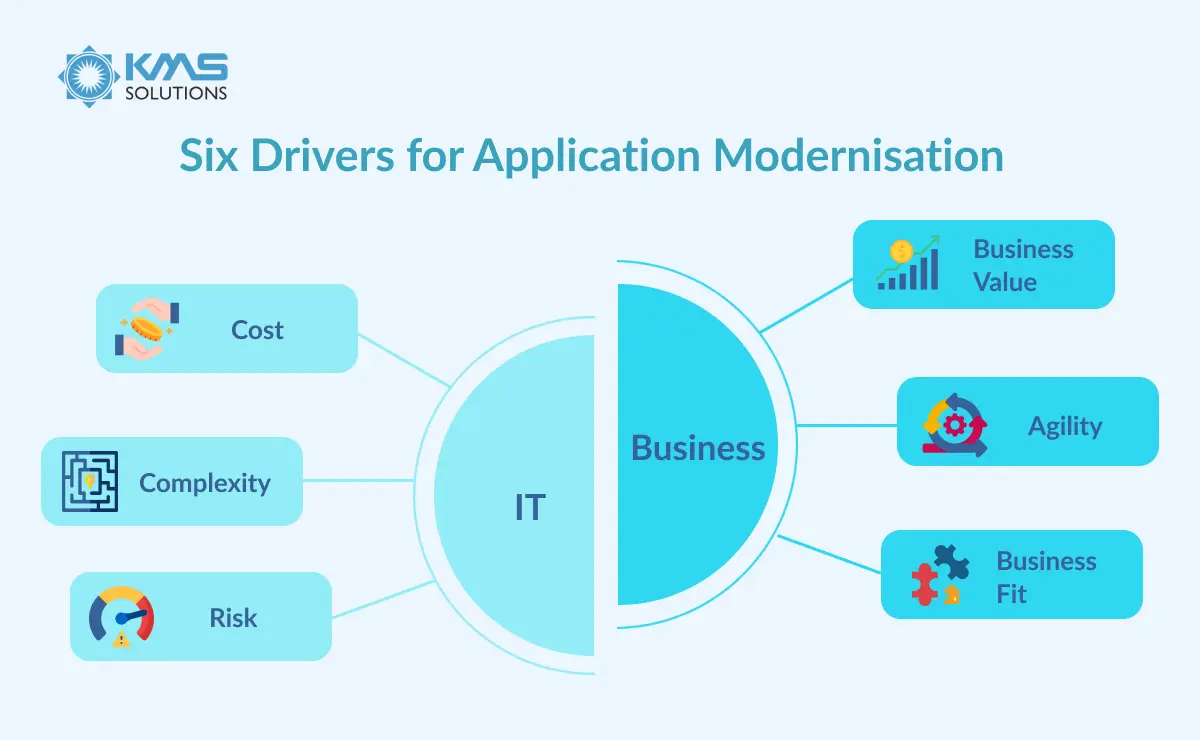

Step 1: Evaluate Your Legacy Banking Architecture

Reflecting on the banks’ previous struggles with outdated systems, Gartner suggests assessing these systems based on each of the six key components:

- Business drivers (Business Value, Agility, and Business Fit): When your existing legacy application fails to align with the evolving requirements of digital enterprises, modernisation becomes imperative.

- IT drivers (Cost, Complexity, and Risk): When the overall ownership expenses are excessive, the technology proves overly intricate, or compromises arise in security, compliance, support, or scalability, then it is time to upgrade.

By conducting a thorough evaluation, banks can make informed decisions about which systems to modernise and how to prioritise their modernisation efforts.

Step 2: Define the Issues

If the current legacy system doesn’t align with the present-day organisational or IT requirements, you will need to refine the problems further. It’s necessary to pinpoint the precise reasons for the inconvenient user experience. This involves concentrating on specific user scenarios.

However, within this strategy, it’s equally important to identify the strengths of the legacy software. Gaining insight into what works and what doesn’t in the obsolete banking app to help decide the modernisation approach.

Step 3: Select Your Appropriate Modernisation Approach

There are four options available for modernising outdated banking software. Let’s delve deeper into each of these alternatives.

- Full software replacement

This strategy involves completely replacing the existing legacy banking app with a contemporary solution. Although the full replacement of software might demand additional time and resources, it offers the advantage of starting anew with the latest technologies and prevailing industry standards. This empowers banks to develop a system that is customised to its current requirements, devoid of any limitations imposed by obsolete software.

Pros | Cons |

– Utilisation of cutting-edge technologies and frameworks – Greater alignment with the existing business processes and requirements. – Removal of technical obligations and legacy constraints. | – Significant expenses and resource demands – Possible complexities in migrating data |

- Incremental modernisation

The incremental modernisation process involves the gradual enhancement of different elements within legacy banking software. This method helps mitigate the risk of complete system failure and enables the bank to uphold essential functions while enhancing other areas. It serves as a pragmatic and efficient approach to updating software systems without disrupting the bank’s daily operations.

Pros | Cons |

– Minimised risks and simplified change management. – Adaptability to sequence updates based on business priorities. – Faster introduction of new enhancements without necessitating a complete system halt. | – Potential difficulties in ensuring seamless integration between existing and new modules. – Extended timeline to achieve a fully modernised system. – Risk of accumulating further technical debt if not effectively managed. |

- Service-Oriented Architecture (SOA)

Embracing a service-oriented architecture involves dividing the existing banking app into more minor services that can be updated or replaced independently. By doing so, each service can perform certain functions and interact with others through APIs (Application Programming Interfaces).

Pros | Cons |

– Flexibility in updating separate services. – Enhanced incorporation of third-party services and APIs. – Simplified maintenance and increased scalability. | – More difficulty in overseeing a distributed architecture. – Potential additional performance load due to inter-service communication. – Demands careful strategy to prevent generating closely interconnected components. |

- Cloud migration

Migrating legacy banking software to the cloud can yield numerous benefits, including enhanced scalability, increased availability, and improved cost-effectiveness. Cloud service providers offer a broad spectrum of services that can enhance the software’s functionalities.

Pros | Cons |

– Scalability to handle numerous workloads. – Improved disaster recovery and data duplication. – Decreased expenses for hardware and infrastructure maintenance. | – Potential compatibility problems with current software and integrations. |

As you determine which legacy software modernisation option to embrace, consider your corporation’s particular requirements, budget, and long-term goals.

Step 4: Choose Reliable Technologies and Modernisation Partner

To experience the positive influence of IT legacy modernisation, it is necessary to ensure that your software development team is utilising a reputable and top-notch tech stack for banking app development. The best practice here is to choose technology that matches your product’s distinct characteristics and business objectives.

It’s worth considering working closely with your internal engineering team or seeking advice from an experienced financial services consulting firm. To maximise the time-to-market of your modernisation project, you can look for a dedicated software development team that is proficient in leveraging Agile and DevOps practices and has expertise in re-engineering technology for BFSI organisations.

Step 5: Outline a Post-Modernization Strategy

Implementing software engineering best practices throughout your IT division can prevent you from encountering the same issues that led you to redevelop your existing system. Therefore, clean and readable code, coupled with well-designed component architecture and comprehensive project documentation, will make your banking app effortlessly testable, maintainable, and scalable in the long term.

Furthermore, banks and financial institutions should consider how their employees from different departments will adopt the new system. Since they may require some time and support to become accustomed to the modernised system, you can prepare some workshops and training courses to expedite the process and improve their performance.

Priority Aspects for Banking System Updating

When it comes to modernising legacy banking systems, a software backend is the most affected. Here are some distinct areas that should be considered most:

1. Data Governance & Management Platform

Legacy systems often lead to stranded or uncollected data, hindering banks from effectively competing with other digital players, implementing advanced analytics-based solutions, or experimenting with predictive analytics, AI, and ML.

Incumbent banks cannot perform real-time business intelligence and advanced big data analysis with their outdated system unless they establish a robust data management platform.

Shifting to a unified data platform may significantly enhance data traceability, accountability, and, subsequently, reporting capabilities to assist banking institutions in remaining compliant with the latest industry regulations. Moreover, this also makes the payment system architecture become more resilient to security vulnerabilities.

2. Data Migration and Transformations

When it comes to modernising an older system, data migration is the most crucial step in guaranteeing the integrity of all existing data. Cloud computing has made substantial leaps in terms of effectiveness, affordability, and security, resulting in new opportunities for banks.

One clear motive for transitioning to the cloud involves the substitution of outdated and challenging on-premises legacy systems, along with the release from the expensive cycle of equipment replacement and upgrades.

Transitioning to a variety of cloud services and delivery models such as SaaS, IaaS, and PaaS can enable you to progressively unbundle your legacy software without significant operational disruptions. A roadmap for data migration on the cloud includes:

- Laying a cloud foundation

- Assessing your app portfolio

- Planning your data migration

- Transforming and validating the data

- Conducting testing and acceptance

3. IT Architecture Optimization

In fact, it might not be practical for the majority of banks to completely step away from the legacy core banking systems due to the elevated risks involved. In these instances, an alternative approach is to systematically disentangle and modularise a banking IT architecture. A robust IT governance process is necessary for a successful evolution. This includes:

- Reduction of duplication and unnecessary processes

- Ensuring that your company goals and technical competencies are well-aligned

- Building a standardised technology portfolio, which is easier and considerably cheaper to maintain

- Adopting a cohesive strategy for risk, compliance, and security management.

4. DevOps/SecOps

While it’s essential to disentangle legacy systems, the software development process should, conversely, be consolidated to achieve enhanced performance.

DevOps, at its core, is about connecting your development, operations, and quality assurance functions. Implementing DevOps practices can accelerate the release of new products to the market without compromising their quality.

The key principles of DevOps that you should follow are:

- Establish more operations and QA during the early stages of the software development lifecycle (SDLC) to reduce the risks of costly rework after that.

- Adopt automation testing in the development and delivery pipelines to reduce bottlenecks and accelerate the process.

- Consider core software metrics, comprising deployment frequency, delivery lead time, time to recovery, and change failure rate.

- Gather feedback, review metrics, and continuously invest in additional process improvements.

SecOps is the next step for banks striving to fulfil security by designing compliance mandates, the logical progression. Incorporating security testing at the outset of the application development process can significantly reduce the likelihood of security breaches in deployed products, thereby averting costly penalties.

Conclusion

Modernising legacy banking systems is no longer an option but a necessity for banks to stay competitive in today’s digital landscape. By following the essential steps outlined in this article, banks can revolutionise their legacy bank online and provide a modern and seamless banking experience to their customers.

Now is the time for banks to embark on the journey of modernising their legacy banking applications. By doing so, they can revolutionise their online banking services and provide their customers with a banking experience that is secure, convenient, and personalised. If you have a plan to revolutionise your legacy bank online and modernise your banking apps, contact us today for a consultation. Our team of experts will guide you through the essential steps and help you achieve a successful modernisation.