Closing the year 2021, the banking sector has managed to turn the pandemic into growth opportunities. Most domestic banks have achieved 20% pre-tax profit growth despite the unprecedented challenge brought by Covid-19 being at its peak. That’s good news, a clear sign that digital transformation can safeguard banks against the current uncertain and volatile landscape.

In this article, let’s examine some of the most prominent digital banking trends for 2022.

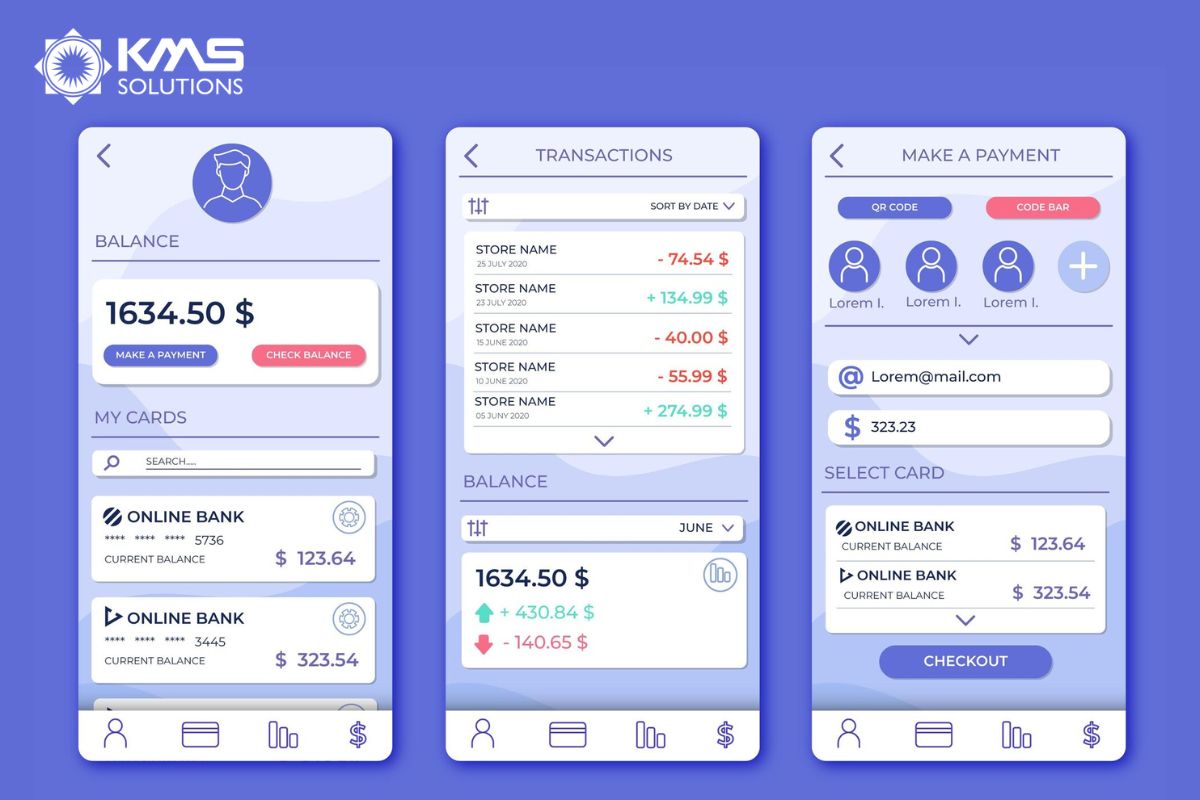

1. Focusing on Banking UX

Back then, banks look at UI/UX merely as a marketing aspect of their digital products rather than a core part that reinforces all features and experiences that users have with the bank. But recently, a market threat called fintech companies has changed all that. With their user-centric and simple-but-not-simplistic product design, fintech forces banks to rediscover the value of a cleverly designed interface and user experience.

Bad banking UI/UX is partly why today’s customers are disappointed with banks. A survey by GMS Software Technology points out that 73% of respondents feel that banks do not value their customers.

In 2022, all banks’ digital strategies need to be driven by UI/UX, guided by these dominant trends

- UI/UX embodies the bank’s promises. Banking UI/UX is beyond pleasing logos and color schemes. The best banking UI/UX design reflects the bank’s personality by communicating with users in a unique voice and tone. More importantly, it achieves that without compromising customers’ trust and security.

- Consistent experience across the ecosystem. Banks should be able to deliver the same brand experience across all channels, whether it’s in-branch, mobile apps, or ATMs. This is more about strategies and less about technologies, requiring additional investments into marketing efforts.

- Human-centric banking experience. Banking UI/UX is not just about fast transaction processing. Today, it must be about delivering meaningful engagement that’s relevant to users’ life and preferences. This can be achieved through a design method called Design Thinking, coupled with advanced analytics technologies.

2. Embedded Finance will be everywhere.

Embedded finance allows banks to embed products directly into other non-financial platforms to promote and provide their digital services such as P2P Payment, Buy Now Pay Later, Digital Lending, or Financial management.

A report by Lightyear Capital predicted that the embedded finance market will contribute $230 billion of revenue by 2025, which is a tenfold growth compared to 2020 ($22.5 billion).

Potential partnerships for embedded finance could be the e-commerce sites, ride-hailing apps, streaming services, or e-wallets that modern consumers cannot live without. Behind embedded finance are a Banking-as-a-Service (BaaS) and Open Banking infrastructure. Thanks to embedded finance, banks can now promote their products on these popular platforms and explore new revenue streams at a meager cost.

According to Galileo’s findings, consumers have become more receptive to financial services offered by non-financial companies.

In 2022, the boundaries between pure banking services and non–banking ones will keep blurring. Already, non-financial players such as Grab or Shopee have entered into partnerships with fintech companies to embrace embedded finance. Banks cannot afford to ignore this trend. Embedded finance can be an opportunity for banks to be involved in customers’ every aspect of life.

3. Open Banking will continue to expand.

More and more banks are opening their data, allowing third-party companies to access customers’ transactions and financial data – with customers’ permission. Across the BFSI landscape, we can see more APIs are being built, and partnerships signed to enrich banks’ ecosystems.

Open banking has been the foundation of most banking innovations today. In 2022, more digital banking trends will come from open banking. Even Forrester agrees. In Forrester’s latest blog, the enterprise predicts that next year will witness more banks taking an open, collaborative approach to their platforms. By integrating data from third-party partners, open banking helps banks deliver more value to their customers while achieving a holistic view of customers’ finances.

4. Physical channels are still important.

The ongoing pandemics with branch closings and consolidations lead many banking executives to think that physical channels no longer work. Still, in the competition against digital-only financial institutions, brick-and-mortar can help banks stand out.

Because, in fact, people still want physical channels. In a survey by Deloitte, 64% of Baby Boomers, 54% of Gen Xers, 48% of millennials, and 58% of Gen Z said they would choose to visit physical branches when opening accounts. Also, according to a report by Financial Brand, up to 80% of customers say they visited bank branches in the last year, and 35% do that at least monthly.

The most substantial reason is trust. People feel closer to physical branches since they have existed since the very first day of bank. It’s a place where people can come down to take out real cash and talk to real people. While digital-only banking services save time and money, people are not ready to trust those emotionless algorithms fully. And when problems happen, they want to complain face-to-face to humans, not a chatbot.

In addition, the bank branch still is a space for maintaining brand identity. Having an eye-catching branch or headquarter on a busy road or shopping district will differentiate your banks from the digital-only counterparts that exist only online.

5. Customer verification will move away from SMS

Thanks to the convenient contactless mobile technologies, customers can perform transactions online without having to be physically present at banks’ branches.

The problem is how banks can authenticate the identity of these “digital customers”.

Conventionally, banks use OTP via SMS to ensure customers are who they claim to be. But it has been proven times and again that this method is not secure at all. SMS has numerous technical vulnerabilities, which fraudsters can easily exploit and hijack customers’ confidential information through their clever schemes using social engineering, phishing, … Even Microsoft concurs that SMS is the worst regarding digital security.

In addition, SMS is prohibitively costly. It is reported that 11,000 billion VND is what the 4 state-owned banks have to spend every year on sending SMS.

The future of digital banking will need integrated and more secure customer verification technologies. And eKYC (electronic Know-your-Customer) is one of them. Today’s eKYC solutions are integrated with digital signatures, liveness detection, biometric authentication, face matching, fraud prevention, and OCR (Optical Character Recognition). These features make sure that banks can accurately verify customers and provide a seamless digital experience while not compromising security.

6. Digital Banking drives Financial Inclusion.

In 2017, up to 1.7 billion adults were unbanked, according to World Bank. Digital banking tools such as mobile apps and web portals allowed people without access to branches or ATMs to enjoy formal financial services, such as securities, payments, credit, savings, and insurance.

Also, according to a recent study cited by the U.N. Environment Programme, enhancing financial products’ affordability, availability, and accessibility can increase 14% GDP in developing countries and 30% in developed ones.

Next year in 2022, digital banking will continue to be the strongest force for financial inclusion worldwide. People in many lower-income areas have started to use mobile phones to send, receive, and manage money. During economic crises, digital banking tools can help people stay resilient.

7. Integrating financial wellness into digital products

Aside from the big corporations and VIP clients, banks also have middle- and low-income customers. They can struggle to pay bills and save money. Part of the reason is that nobody gives them financial advice. According to the Result of Vietnam Household Living standards, monthly income in urban and rural areas are respectively 5.7 million VND and 3.9 million VND.

Financial wellness and financial education are not just a matter of customer experience. It’s an essential part of the larger economy and society. More than any industry, banks are responsible for providing financial wellness support to customers. Successful wellness programs can only make banks appear more trustworthy and accountable in the public’s eyes. Fortunately, this has become easier than ever with digital tools.

Socially responsible banks are doing this by integrating financial wellness features into their mobile apps, where customers can set and progress to their individual financial goals. An example is from a foreign bank – Bank of America’s Life Plan. By October 2021, one year after the program was launched, Life Plan has attracted more than 5 million users. Moreover, Bank of America now has 1 million appointments from those customers. This shows how digital tools with financial wellness can help banks improve digital and personal interactions.

8. ESG Banking Products will be more popular

Banks are under increasing pressure from consumers and environments to responsibly follow environmental, social, and governance (ESG) principles. In addition, banks are also demanded to design eco-friendly products and services – the so-called green banking – to fight climate change.

One popular trend in green banking is carbon footprint tracking. Many eco-conscious banks are launching carbon tracking features into their mobile app. It displays and gives customer reports on their purchases’ carbon impact.

Today’s generations care more about the environment. A Carbon Trust survey revealed that 67% of consumers support carbon tracking, and 64% perceive brands more positively when they can prove that they are reducing their products’ carbon footprints.

In 2022, digital banking features that help customers make better-informed choices about how their spending affects their carbon footprints will become more prevalent. When banks enable consumers to see the climate impact of their everyday spending, they can be empowered to make greener choices.

Conclusion

2020’s digital banking trends are not just about investing in new technologies. They are also about transforming banks’ operations, customer experience, and even cultures to thrive in the increasingly digital world.

At KMS Solutions, we’ve helped various leading banks to accelerate their digital transformation and scale digital capabilities. Contact us now to have our subject-matter experts develop an effective digital strategy tailored to your business.