Establishing secure data-sharing systems that require customer consent is essential for countries to unlock their future economic potential. Governments worldwide have increasingly recognized this necessity and begun implementing it, primarily commencing in the banking industry, through the development of ‘Open Banking’ frameworks. Indeed, the global open banking market is anticipated to increase from US$15.13 billion in 2021 to US$123.70 billion by 2031, expanding at a CAGR of 23.4%, as per Forbes.

Open banking is gaining traction across the Asia-Pacific region. However, the journeys to implement these policy directives in different countries and regions are taking vary considerably. They can range from market-driven to regulator-led or even a hybrid that combines elements of both.

In this article, we will examine two countries in the region to provide an overview of their open banking progress: Australia and Singapore.

Open Banking Deployment Strategy

Australia

Australia is one of the only markets in Asia-Pacific that is unambiguously regulator-led. The country’s Consumer Data Right (CDR) was enacted in mid-2019, legalized and made mandatory open banking across the financial services industry.

The CDR is an economy-wide data-sharing regime, while open banking is a compulsory framework that facilitates the secure sharing of banking data by both individuals and businesses with third-party entities and allows these third parties to initiate payments on behalf of the data owner.

Singapore

In contrast to Australia, Singapore is considered a market-driven jurisdiction for open banking. Although regulators in Singapore have generally not mandated banks to implement open banking, the Monetary Authority of Singapore (MAS) has nonetheless played an essential role in the country’s open banking process.

The MAS became the pioneering regulatory body in the Asia-Pacific region to issue directives on open banking and establish a roadmap for the provision of banking data through open APIs. It also manages the financial industry API register, which monitors open APIs in Singapore’s financial sector categorized by their functionalities.

Customer Perspectives on Open Banking

-

Australia

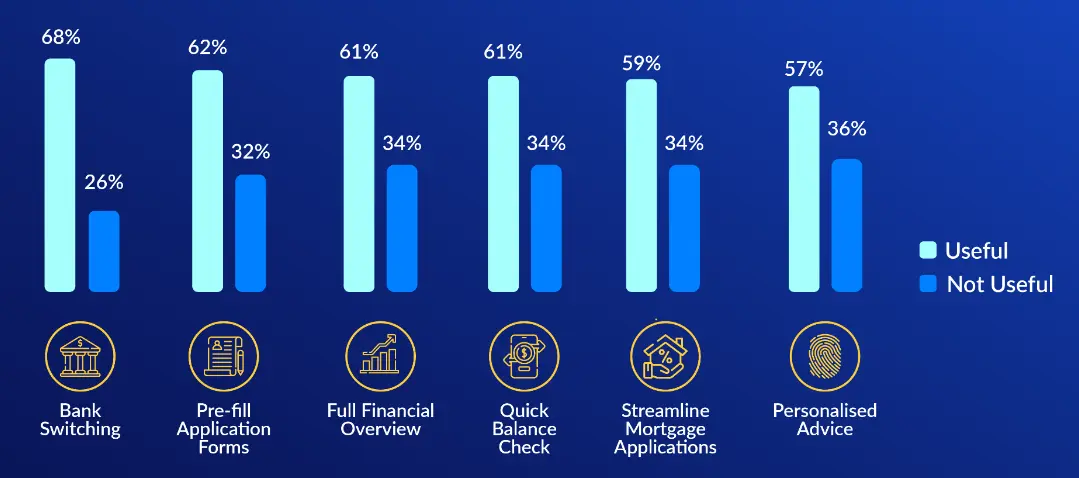

In the KMS Digital Banking Industry Report, we realized that most Australians consider open banking-powered products and services as useful.

- 59% of respondents believe linking their bank account to share financial data and get access to personalized products will help streamline their experience.

- Australian customers also prioritize privacy, security, and control when sharing their financial information with third parties.

- The consumer perspective report of Frollo indicates that while banks are the most trusted institutions to share their data (51%), big technology companies (27%) and fintech (23%) are the least trusted ones.

- Millennials and Gen Z are likely the first to get on board.

Singapore

Customer expectations in Singapore are evolving rapidly, demanding more personalized and convenient banking services.

- In 2022, 99% of customers in Singapore considered open banking either a ‘must have’ or ‘important’.

- The KMS report above also indicates that approximately six in ten respondents were willing to share substantial personal data, including income, location details, and lifestyle information, to their banks and insurers in return for more streamlined and personalized banking services.

How Banks in Australia Adopted The Trend of Open Banking

-

A deep focus on data holder standards:

According to Frollo, in 2023, nearly all banks are sharing data for more than 30 distinct financial products, and the number of entities utilizing this data has doubled in the past year.

Under the circumstance where the CDR is still relatively nascent, uptake has been fairly slow. There are 76 data holders and 32 accredited data recipients on the register, only 20 of which have an ‘active’ status, according to the research of NAB and Natwest. To sustain the open banking ecosystem, it is essential to prioritize enhancements in data quality and adhere to data holder standards to ensure a dependable and user-friendly experience.

-

Leading banks have already initiated API experimentation:

APIs form the backbone of open banking, serving as the driving force that enables connectivity to be central to banking strategies with profound and enduring business implications. Many leading banks have initiated API utilization to create a new ecosystem and products, enhance customer service, and expedite their time-to-market.

- In 2021, the National Australia Bank (NAB) became the first major Australian bank to launch an Application Programming Interface (API) Developer Portal as part of its commitment to improving customer experiences through collaboration.

- Up, a digital bank that operates under Bendigo and Adelaide Bank’s ADI, leverages open banking APIs to offer customers real-time transaction information, automated categorization of expenses, and personalized spending insights.

-

Fintech startups are embracing API-driven innovation:

B2B fintech startups and digital banks are swiftly seizing the opportunities presented by open banking. These agile startups are concentrated on creating distinctive and inventive value propositions by collaboratively addressing specific banking and customer challenges through extensive partnerships and the utilization of B2B APIs or open APIs.

The Impact of Open Banking on Singapore’s Financial Sector

-

A strong foundation for open banking:

Additionally, MAS has introduced APIX, an API guidance and collaboration platform. Besides, it fostered a secure environment that promotes and sustains innovation through regulated sandboxes. These sandboxes are designed to empower service providers to experiment, iterate, and bring their offerings to market more expeditiously, all while ensuring that the services they provide enhance efficiency, risk management, and people’s lives.

-

Singapore Banks have concentrated on building ecosystems for their users:

Several major banks in Singapore, including DBS, HSBC, Standard Chartered, and Citi, to mention a few, have proactively utilized APIs by either becoming part of third-party ecosystems or establishing their own marketplaces. They are committed to providing a seamless experience to their banking customers and API consumers.

For instance, DBS has expanded this seamless experience beyond users and integrated its partners by operating a developer portal featuring a diverse range of over 200 APIs. The report from Forrester also indicates that this initiative has facilitated innovation in areas like payments and loans through collaborations with companies like Grab, PropertyGuru, and McDonald’s.

-

Digital players will drive banks to adopt innovative open banking approaches:

The banks in Singapore are recognized for their active collaborations and diverse approaches to market expansion, establishing themselves as open banking pioneers in the Asia Pacific region.

However, they have mainly relied on third-party partners to generate new user value, offering open APIs for innovation. With the introduction of Financial Planning Digital Services (FPDS) and digital banks, there is a growing need for Singaporean banks to assess their unique value proposition and open banking strategy.

The Future of Open Banking in the Asia Pacific Area

The report from NAB and Natwest indicates that although there has been encouragement for the adoption of open banking in the APAC region in recent years, in comparison to other areas such as Europe and the US, this sector is still at a very early stage of development.

Core banking legacy systems, with their rigid, closed architectures, frequently do not align with the requirements of the digital age and hinder banks from fully achieving the benefits of open banking and adapting to the broader open finance trend. To tap into new business prospects and remain pertinent in the dynamic digital landscape, undergoing digital transformation is an indispensable prerequisite for banks.

Open Finance

Open banking marks the initial phase in the transition toward an open data society, a data-centric realm that connects various ecosystems, spanning from finance to technology, empowering consumers to take full control of their data streams, leveraging them for personal benefit.

Another significant milestone in this evolution is open finance, an expansion of open banking that broadens the spectrum of consumer financial data shared, offering a more comprehensive and accurate view of an individual’s digital financial footprint.

While open banking and the broader open finance landscape bring competitive challenges for banks, they also equip them to compete with emerging digital-first competitors. Moreover, it allows banks to meet the growing demand for seamless and hassle-free digital services while enhancing their financial performance.

System modernization options

According to Forbes, in the realm of system modernization, banks have three viable options: Rip-and-replace the existing core, take a gradual journey-led transition approach, or build a standalone greenfield cloud-native stack alongside their existing core.

Sum Up

Open banking in the APAC region, especially Singapore and Australia, is on an upward path, with expectations of growing adoption and continuous evolution. While there are numerous prospects for the creation of new business models and improved customer experiences, it’s critical to tackle challenges like data security and the integration of legacy systems.

In this dynamic era of open banking, effective partnerships, and adaptive solutions are critical. KMS Solutions is ready to help banks and financial institutions in the APAC region navigate these challenges as a technology-trusted partner. If you aim to remain at the forefront of this revolution and unlock the complete potential of open banking, don’t hesitate to connect with us.